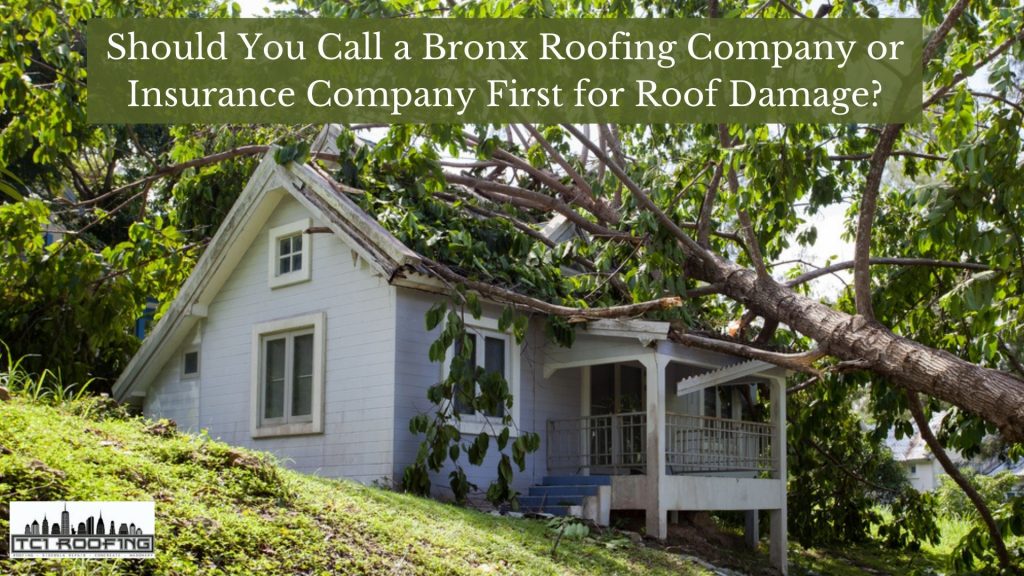

So you’ve noticed roof damage on your roof and now need to figure out what to do. You could call up a residential roofing company or an insurance company first. Which should you do? If you’re unsure, this blog post will help answer that question! We’ll discuss the difference between roofing services and insurance companies, as well as how they work together with one another to get your roof repaired.

Should You Call Your Insurance Company or a Roofing Contractor First For a Storm-Damaged Roof?

If you feel an intense storm has damaged your roofing in your neighborhood, the first thing you should do is contact your homeowner’s insurance company. What happens once you’ve given them all of the necessary information is determined upon your location and the insurance company you choose.

Some insurers dispatch an adjuster to do roof inspections, assess the damage, and determine whether or not you have a claim. It’ll be time to start looking for a good roofing company if they approve your claim after their examination.

Before assigning an adjuster, some insurance companies may advise you to have a roofing specialist do a roof inspection for damage. This happens all the time in Manhattan, but you won’t know unless you contact your homeowner’s insurance carrier.

Regardless of the scenario you find yourself in. You should first call your insurance company if you anticipate storm damage.

What Are The Things That You Should Know About Hiring a Roofing Contractor For Your Insurance Claim

You now know that you should call your insurance company before contacting a local roofing company. However, there are a few things to look out for when it’s time to hire a roofing contractor for your insurance claim.

The Roofing Company Must Have Experience Working With Insurance Claims

When you’re ready to start looking for a roofing contractor to handle your insurance claim, you’ll need to conduct some research. Throughout your research, the first thing you should look for is whether or not a prospective roofing company has ever dealt with an insurance claim.

Roofing companies that deal with insurance claims are familiar with the procedure, know how to interpret your claim, fight to ensure that everything on the insurance estimate is proper, and know how to do the work per your insurance company. A roofing contractor that works with insurance regularly may also assist you in avoiding insurance fraud unintentionally.

Consider the case below:

You may find yourself in a situation where the work estimate is less than the amount the insurance company agreed to pay if you have a Replacement Cost Value policy (your insurance company pays for your roof repair or roof replacement). You are not permitted to keep any leftover funds.

Your RCV policy requires proof of completion to demonstrate that the items listed in the insurance estimate were also included in the contractor’s scope of work. Suppose you ask for a check for recoverable depreciation (the amount an insurance company believes a roof has depreciated over time) but do not complete the job. In that case, your insurance company will not pay you the depreciation.

Hiring a roofing contractor familiar with insurance claims could make for a pleasant experience in an otherwise stressful circumstance.

You Need to Make Sure The Roofing Contractor is Local to Your Area

When looking for potential contractors to hire, it’s vital to choose local to your area, especially for insurance work. They must have a physical location and a phone number in your area with a local area code.

This is the case because many out-of-state companies (storm chasers) come in after a major storm and undercut the prices of local roofing companies in your area. Then, they’ll send highly trained salespeople to go door to door and use scare tactics to sell new roofs to naïve homeowners.

After receiving the funds, the personnel stays to finish the work before moving to the next storm-affected area. Unfortunately, the work on these roofs is usually done incorrectly, with little concern for local codes or whether your shingle roof is properly placed.

If your roof sustains storm damage, contact a reputable licensed roofing contractor in your area to ensure that this does not happen again when a large storm passes through.

Ask To See The Potential Roofing Company’s Paperwork

A roofing and siding contractor who is licensed, bonded, and insured is essential. These three pieces of paper are there to protect you and make sure the task is done appropriately.

You should demand proof that the roofing company in your state is fully licensed, bonded, and insured. You and your roof are at risk if even one of the three is missing.

However, how critical is this paperwork to you?

Licensed

To receive a license, a contractor needs to register with the state board of licensing contractors. After that, the cost of the job will decide the type of license they’ll need.

For jobs above $3,000, a home improvement license is necessary, and for jobs over $25,000, a general contractor’s license is required.

Roofing contractors should have a general contractor’s license because a new roof is such a large investment.

Bonded

The consumer can turn to the bond firm for assistance if a company goes out of business in the middle of a task or an issue with the work they do not solve.

A bonded roofing contractor has demonstrated to a bonding company that they operate legally and ethically. The bond is posted because the bonding business is sure that the contractor will complete the task correctly.

Insured

All contractors should have general liability, workers’ compensation, and company vehicle insurance on all owned and unowned vehicles.

The contractor’s general liability insurance and workman’s comp limitations are determined by the size of the contractor’s jobs and the state in which they are located. Their overall liability will be lower if they only conduct minor residential work rather than major projects.

Employing a roofing contractor that isn’t licensed, bonded, and insured in your state. If something goes wrong, you’ll be left with no recourse. So make sure that you always choose the best roofing company who can carry out the job correctly and take care of your roofing needs! We at TCI Manhattan are delighted to help and assist you whether you need roof repairs due to roof leaks or residential roof replacement. Contact us today!

Show Your Roofing Contractor Your Insurance Estimate Paperwork

You’ve just learned three crucial factors to think about when choosing a roofing contractor to handle your insurance claim. But what happens if you’ve found one that fulfills all three of the criteria mentioned above?

The initial step is to give them all of your relevant insurance documentation. Some homeowners are afraid to tell their roofing company about their insurance claim estimate, but it is vital.

You’re probably thinking now, “Why is it so important?”

“We broke everything down for you because we want you to have a complete understanding of the insurance process.”